The No Surprises Act arbitration system is producing results Congress never intended — and the fix isn’t more rules. It’s better data.

A plastic surgeon in New York just won $440,000 in a single arbitration case for a breast reduction his own website advertises at $15,000 to $25,000. He’s won more than 85% of his 6,000+ arbitration filings. He is not alone — doctors filed 1.2 million arbitration claims in the first half of last year, roughly 70 times what Congress projected for an entire year, and they’re winning 88% of them.

The New York Times reported all of this. The framing, predictably, was about doctors gaming the system and insurers passing costs to consumers. Representative Pallone, one of the law’s architects, called for reform. Karen Ignagni at EmblemHealth called it “a recipe for driving up health care costs.”

They’re not wrong. But they’re also not diagnosing the real problem.

The No Surprises Act Arbitration Data Everyone Is Missing

The No Surprises Act arbitration system — formally called the Independent Dispute Resolution (IDR) process — is a baseball-style arbitration. Each side submits a number. The arbitrator picks one. No middle ground. No appeal.

That design only works if the arbitrator has a credible way to judge which number is closer to the truth. Congress did anticipate this. It built in the Qualifying Payment Amount (QPA) — the median in-network rate for the service — as the presumptive anchor the arbitrator should start from.

So why isn’t it working? Because the QPA has three structural problems that the public conversation largely ignores:

1. Every plan calculates its own QPA from its own narrow network data.

That means every QPA a plan brings into arbitration reflects what that plan negotiates, not what the market pays. Arbitrators have no way to tell whether a plan’s QPA is credibly benchmarked or conveniently low.

2. Arbitrators are not required to defer to the QPA.

A 2022 federal court ruling struck down the “rebuttable presumption” that the QPA was correct. Arbitrators now weigh it alongside any other factor either side submits — provider experience, case complexity, “usual and customary” rates, whatever the brief argues.

3. Providers bring aggressively-briefed narratives.

Plans bring formulas. As one provider-side attorney told the Times, arbitrators experience “reverse sticker shock” at how low plan payments are and gravitate toward the provider’s number “even if they do seem eyebrow-raisingly high.” In a decision environment with no shared truth, the side that tells the better story wins.

Put those three together and you get exactly what the data shows: an 88% provider win rate, awards multiple orders of magnitude above historical out-of-network rates, and plans that are effectively bringing pocket calculators to a courtroom.

.

Reforming the procedure without fixing the underlying information vacuum is like adding more referees to a game with no rulebook.

.

Not a Policy Problem, An Information Problem

The instinct in Washington right now is to legislate tighter arbitration rules — stricter eligibility, limits on filing volume, penalties on the arbitrator firms themselves. Some of that is warranted. Medicaid and Medicare Advantage claims should not be flooding the IDR system, period.

But tighter procedure rules don’t solve the underlying question the arbitrator is being asked: what is this procedure actually worth?

Without a credible, market-wide, evidence-based answer to that question, every arbitration is a coin flip weighted toward whoever briefs more aggressively. The arbitration firm gets paid per case. The doctor gets paid per win. The plan gets a bill and a premium hike.

Reforming the procedure without fixing the underlying information vacuum is like adding more referees to a game with no rulebook.

What a Real Price Anchor for NSA Arbitration Looks Like

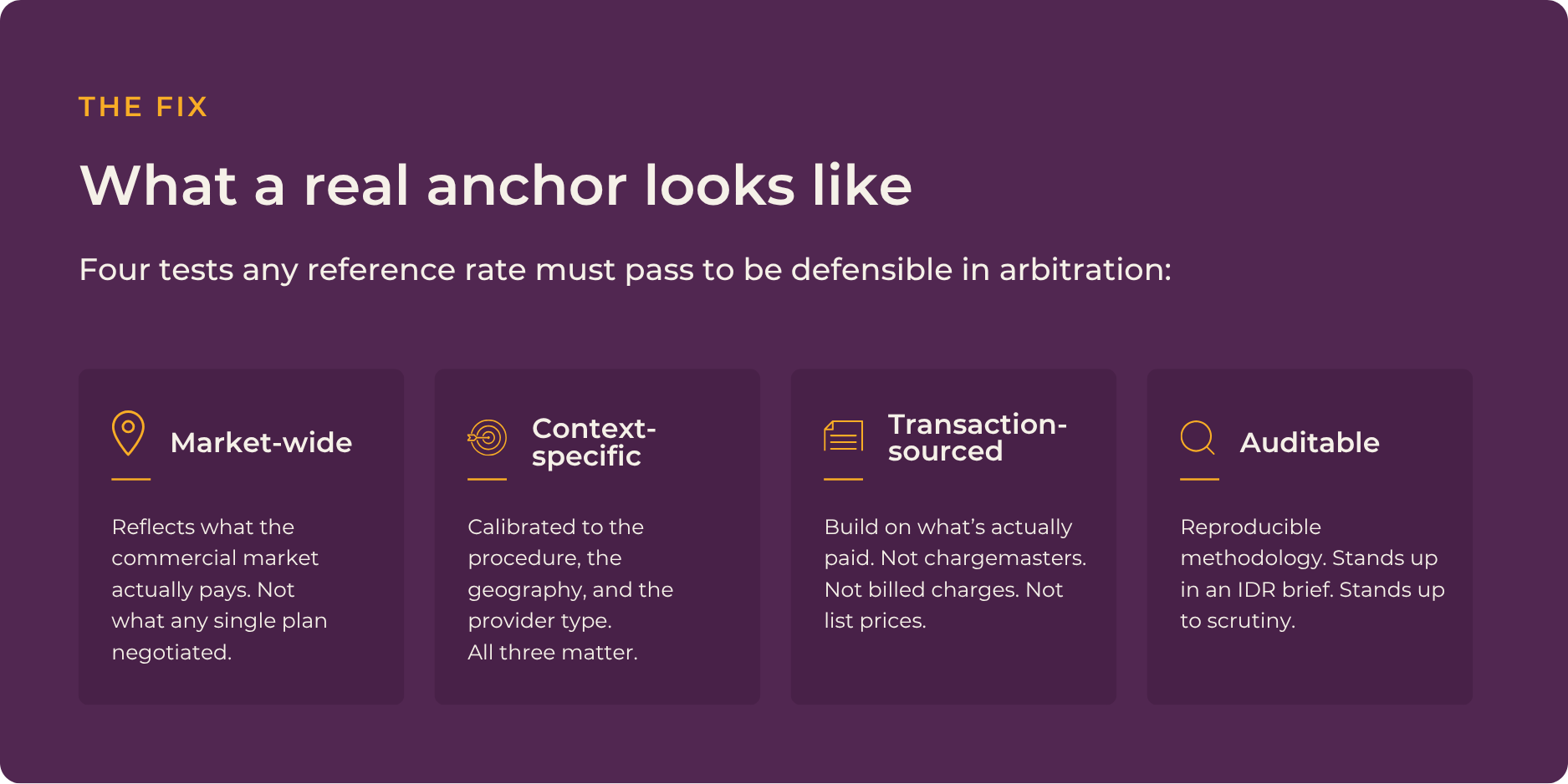

If the goal is to give arbitrators — and everyone upstream of them — a defensible number to work from, that number has to meet four tests:

1. Market-wide, not plan-specific.

It has to reflect what the commercial market actually pays, not what any single plan has negotiated.

2. Procedure-specific, geography-specific, provider-type-specific.

A breast reduction in Manhattan performed by a board-certified plastic surgeon is a different economic event than one in Des Moines performed by a general surgeon. The anchor has to know the difference.

3. Sourced from actual transactions, not list prices or chargemasters.

The Transparency in Coverage Rule exposed the chasm between what providers bill and what the market pays. An anchor built on billed charges is an anchor built on fiction.

4. Continuously updated and fully auditable.

If a plan is going to cite the number in an IDR brief, it needs to stand up to scrutiny. If an arbitrator is going to rely on it, the methodology needs to be reproducible.

This isn’t a hypothetical wishlist. It’s the specification TALON built against when we designed UAPA™ — Universally Acceptable Payment Amount, now patent pending.

How UAPA™ Works

UAPA™ is an evidence-based reference rate derived from a weighted average of actual commercial claims across 400+ payers and 44.5 million shoppable prices. It’s not a median. It’s not a Medicare multiple. It’s not an internal network rate projected outward. It is the observed, transacted market price for the same procedure, in the same geography, at the same provider type — calculated fresh from the transparency data the federal government already mandated that health plans publish.

That distinction matters in an IDR proceeding. When a plan walks into arbitration with a QPA calculated from its own limited in-network data, it is vulnerable. When a plan walks into arbitration with a QPA and a UAPA™ anchor that shows the weighted commercial market rate for that exact procedure in that exact market, the arbitrator finally has the thing they’ve been missing: a credible, defensible, market-sourced answer to what is this procedure actually worth?

And because UAPA™ is built on the same data infrastructure TALON uses to power member shopping, pre-service estimates, and plan-level cost projection, the same reference price that wins in arbitration is the one members see before they schedule care, the one the plan uses to set benchmark reimbursement for its Universal Repricer, and the one the CFO uses to forecast claims spend. The anchor doesn’t live in a silo. It threads the entire cost-of-care workflow.

How UAPA™ Changes No Surprises Act Arbitration Economics

For a TPA or self-insured health plan watching its IDR spend climb, adopting a market-sourced price anchor changes the economics in three ways:

1. Stronger arbitration briefs.

A plan’s IDR submission stops being “here is our network’s median rate” and becomes “here is our network’s median rate, and here is the weighted average the commercial market actually pays for this procedure in this geography, and here is the methodology either side can audit.” Providers currently win by telling a better story. Plans start winning when they tell a story grounded in the actual market.

2. Cleaner QPA math upstream.

TALON’s No Surprises Act Tool automates QPA calculation by procedure, provider type, geography, and CPI-U adjustment, and reprices out-of-network claims via API. When the QPA itself is calculated on clean, properly-segmented data — rather than on whatever the plan’s claims system happened to capture — plans stop losing arbitration cases they should have won on the initial offer.

3. Lower IDR volume over time.

The providers currently filing thousands of speculative claims are doing so because the expected value of filing is positive: low cost per filing, high award amounts when they win, 88% win rate. When plans consistently bring credible market anchors into arbitration and win share flips, the expected value calculation flips too. Filing volume drops. Not because the rules changed — because the economics did.

The Broader Point

The No Surprises Act protected patients from surprise billing. That is a real, durable, bipartisan win and it should not be rolled back.

But the law’s back-end — the IDR process that determines what providers are paid when they decline to go in-network — was built on an assumption that never fully held: that each plan’s internal network data would produce a QPA stable and credible enough to anchor the dispute. It hasn’t. And in the vacuum, every arbitration becomes a negotiation over narrative rather than price.

The fix isn’t only in Washington. The fix is in the data. A market-wide, transaction-sourced, procedure-specific reference price turns arbitration from a coin flip back into an arithmetic problem — which is what Congress intended in the first place.

We’ve spent 11 years building the infrastructure to produce that number at scale. The TiC Rule made the raw data public. UAPA™ makes it usable.

Let’s Talk

If you run a TPA or health plan and you’ve watched your IDR-related spend rise — or you’ve simply stopped tracking it because the losses are too painful to look at — we should have a conversation. TALON’s No Surprises Act Tool and UAPA™ are live with enterprise clients today, and we deploy in 60–120 days.